6 Outdated Investing Rules Making You Poor

You're probably using them right now

You don’t need to be a financial expert to get rich.

But you should be challenging long standing assumptions because what worked 20 years ago doesn’t necessarily work today.

There are certain “rules of thumb” slowly stripping away the wealth you’ve worked so hard to build.

But it’s not the ones you might think. Let’s start with the most common.

The 60/40 rule

Historically asset managers have labelled a balanced portfolio consisting of 60% stocks and 40% bonds. The idea was stocks and bonds move in opposite directions with their performance over the short term, yet they both increase over time.

The allocation was meant to protect investors during market down turns.

During the 2000s and 2010s that relationship held pretty steady but since then we’ve seen a weakness in that correlation. 2022 was a perfect example. Both stocks and bonds got obliterated that year.

The reason for the weaker correlation is beyond the scope of this article.

If you want to know drop a comment below or DM me and I’d be happy to explain.

Another red flag with this strategy is it leaves out an increasingly vital add-on to portfolios: alternative assets. Commodities, infrastructure, private assets are a few examples of beneficial instruments.

Rule of 72

The rule of 72 is meant to determine how long it will take to double your money.

You take 72 and divide it by the return you hope to earn annually and that number gives you the total years it will take to double your money. For example:

If you want a 7% return then we get 72 / 7 = 10.28. Roughly 10 years to double your money.

The problem with this rule is it doesn’t take into consideration taxes or fees. Those factors vary by investor so two people could input the same return target but have different time periods in reality.

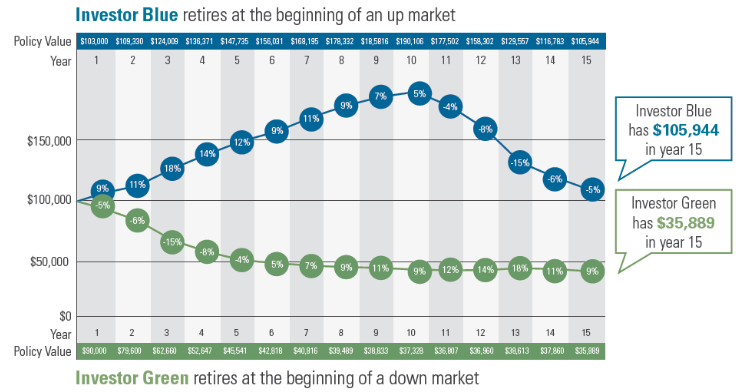

It’s also impossible to predict return sequences. Check this chart below. Both investors experience the same average return just in reverse order. You can see our Blue investor is in a much stronger position because he had gains early on.

Lastly I’ll point out this rule gets even weaker when we look at returns beyond a moderate scale. I’ll use an extreme example.

Let’s say you earn 72% in a year. Well 72/72 = 1. Therefore your money should have doubled in a year on 72% but we know you need 100% to double your money. The rule really starts to lose credibility around 12% annual returns.

If you want more in depth strategies on how to protect your money become a paid subscribe below.

I work with multi-millionaires to protect their assets from fraud, market risk, and taxes.

Paid subscribers get full access to our private chat so you can learn the same methods. This might be one of the only subscriptions that makes you money

The 4% rule

Once you’re retired withdraw 4% of the balance in your retirement accounts every year, adjusting for inflation.

On a $1,000,000 portfolio you withdraw $40,000 year 1, and a little more each year.

Again this rule is susceptible to market return sequences but there’s a deeper underlying problem. The 4% rule was created on a 30 year retirement period. For those that retire early or realize an above average life expectancy there is serious longevity risk.

It also doesn’t account for lifestyle preferences.

If one person wants to watch the grandkids, eat at home, and drive their car into the ground they’re going to need a lot less than someone travelling first class and taking up an expensive hobby.

100 - Your Age

This “formula” is suppose to determine what percentage you allocate towards equities.

If you’re 35 years old then 100 - 35 = 65. You hold 65% equities and 35% in bonds.

There are a bunch of gaps with the idea. First, there is no consideration for your risk tolerance. Some 35 year-olds may be willing to hold 100% equities which means following the formula would leave returns of the table.

The second issue is a lack of investment purpose. If a person is saving for a short term purchase like a house or car, then having those funds in equities is a gamble.

The final issues is the ambiguity of which equities to buy. Emerging markets and Canada have much different risk profiles. So do software companies and utilities. You may follow the formula but still end up disappointed with returns or assuming more risk than you were comfortable with.

50/30/20 Rule

Allocate 50% of your after-tax income on needs

Allocate 30% to wants

Allocate 20% to investing

Following this path can cause issues in a couple ways. It doesn’t factor in the nominal value of your income.

It’s easier for someone earning $250,000 a year to invest 20% than someone making $50,000 because of fixed costs. Housing would likely differ by a meaningful margin however gas, groceries, insurance, cell phone bill, among others would be fairly equal between the two earners.

Here’s the bigger trap:

No definitions of “need” and “want” are provided. One person may think a trip to the Bahamas is a need.

Others may debate if buying your lunch from Subway is a need or a want.

Here’s what to do instead.

Start by investing a small percentage of your gross income. There is no wrong answer. If it’s 1% then it’s 1%. Every 6 months review your budget and see if/how much you can increase your investments.

By starting with your investments instead of needs or wants you are much likelier to actually contribute to your portfolio.

70% of Income for Retirement

We come to our final flawed rule.

There is industry debate on the final number one should use as a percentage of their current income during retirement. The range is 60 - 80% so that’s how we landed on 70%.

If you make $100,000 now then you’ll need $70,000, adjusted for inflation, when you retire.

There are a few drawbacks banking your retirement on the formula.

The most obvious is your income changes over time. You’re not making the same amount at age 25 as you are at 50, at least you shouldn’t be.

Similar to other heuristics we discussed, there is no consideration for your retirement lifestyle. Your lifestyle also affects your investments. Basing your retirement spending on a income percentage today does not factor in your investments or available pension at retirement.

I’ve seen it before where someone makes $200,000 a year in their mid 50s but only has $100,000 in the market.

Following this rule would lead them dangerously astray.

There you have it. Six investing rules of thumb that at worst, need to be put to bed, at best need critical thinking.

If you’re the type of person who thinks before they invest then we’re on the same page. Thank you for reading.